With Lantern as your financial guide, our partnership with Kinsted Wealth helps power a broader, more flexible investment experience behind the scenes.

More room to build. Less reason to settle.

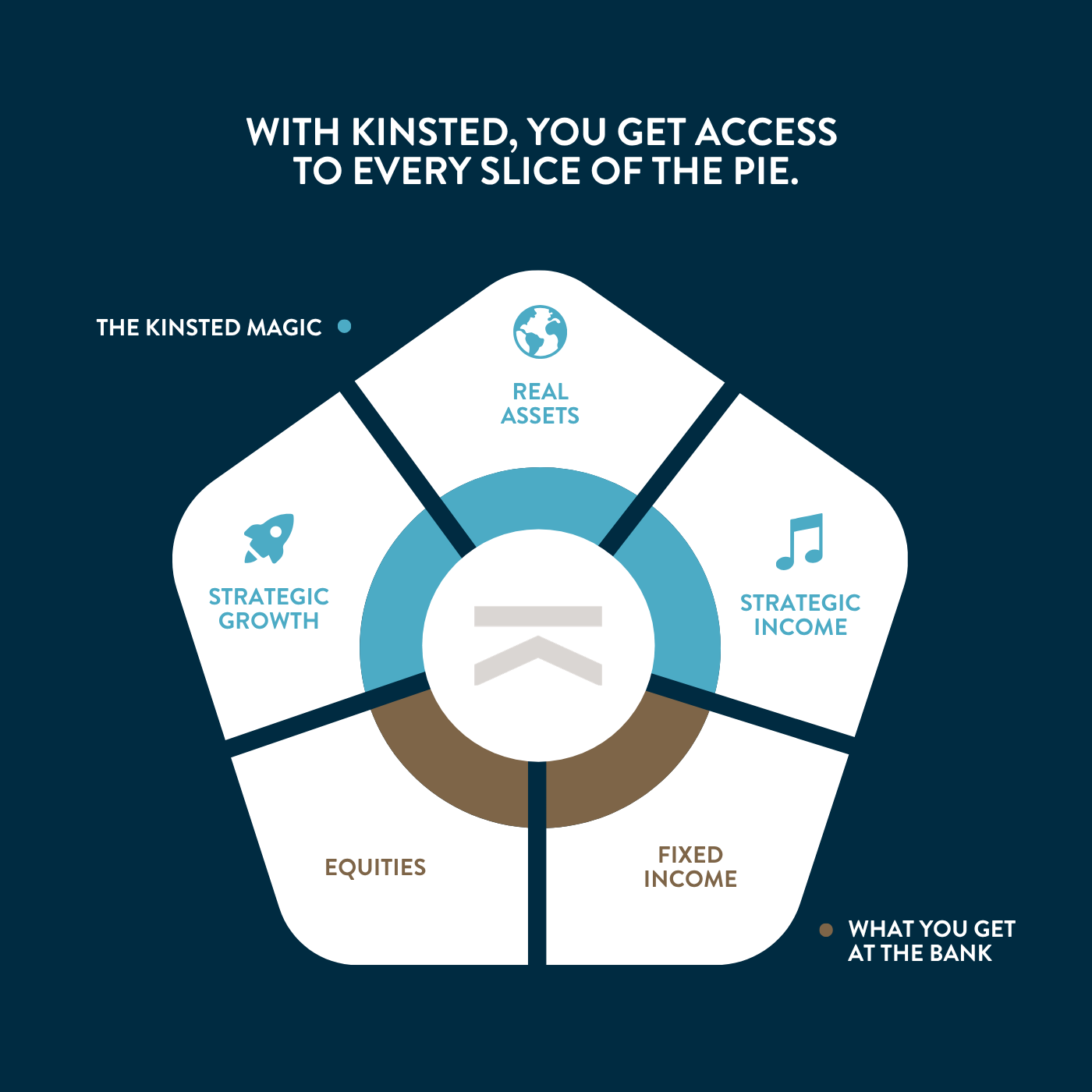

Canada Pension Plan. Harvard University Endowment. CalSTRS. For decades, this is the world institutional investors lived in — a world many families never get invited into.

Many of these opportunities require minimums of $25 million USD or more. That shuts out almost everybody.

Kinsted builds and manages portfolios the way institutions do: disciplined, repeatable, long-term, and not based on whatever product happens to be sitting on a bank shelf this quarter.

In short, you gain access to the kind of investment infrastructure most investors never even get to look at.

Retirement strategy, spending, tax, estate, and family decisions

Ongoing communication and coordination with the rest of your world

A clear relationship that stays human, direct, and accessible

Broader access than a traditional bank shelf

Professional selection, filtering, and rebalancing

A council-based portfolio process instead of one person’s hot take

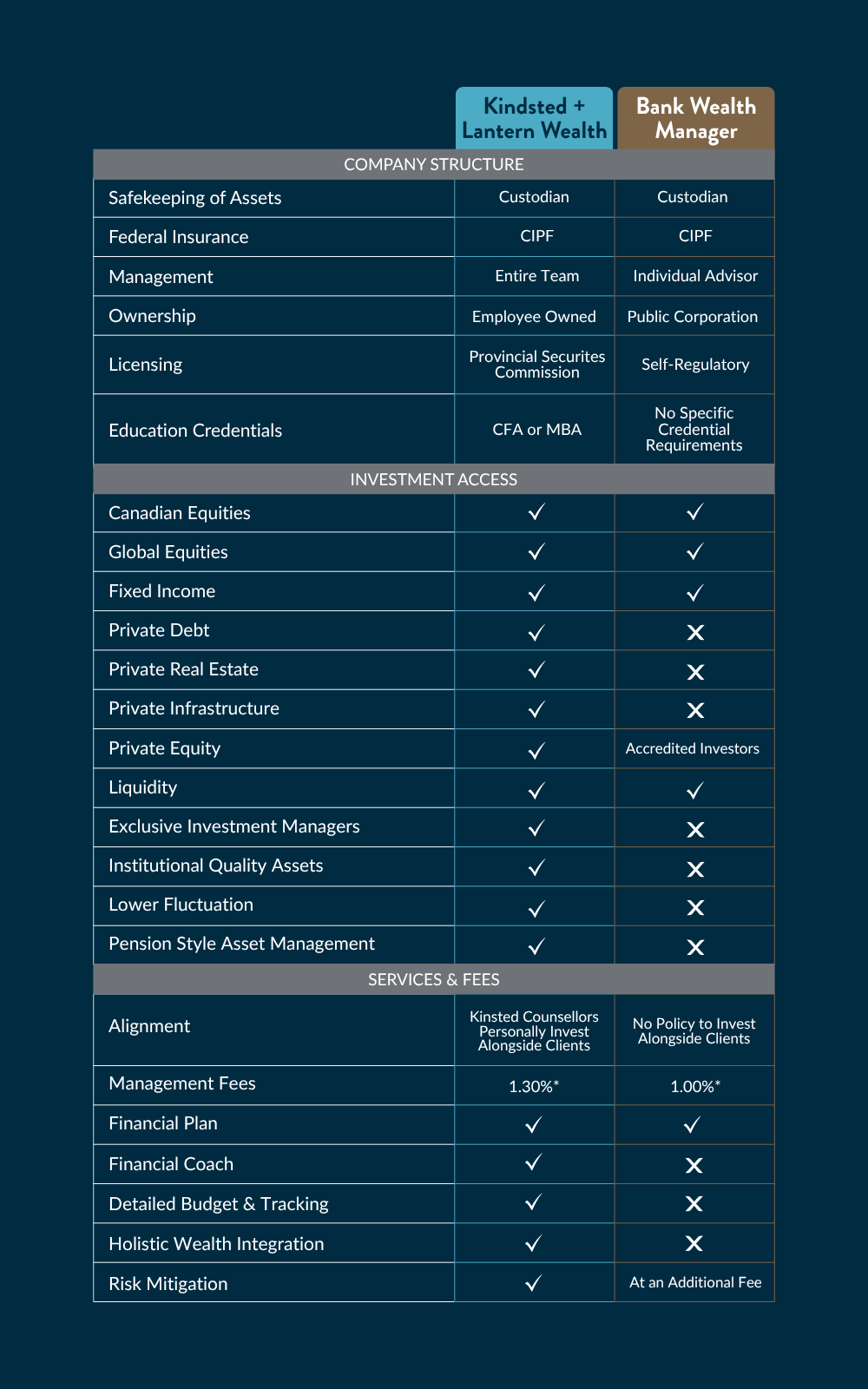

Kinsted is licensed directly with the Alberta Securities Commission and recognized across Canada under the highest regulatory standards, including Ontario. That opens up one of the broadest investment universes available in Canada.

You are no longer choosing only between Canadian stocks, U.S. stocks, international stocks, and whatever a bank decides to put on its menu.

You are choosing from the widest possible pool of opportunities.

You are not choosing from a single shelf. You are choosing from the whole market.

Your assets are held with Aviso Wealth, one of Canada’s major custodians serving credit unions and institutional partners across the country.

Your investments remain independently held and fully transparent. If Kinsted Wealth or Lantern Wealth were ever to cease operating unexpectedly, your assets would still remain safely held at Aviso.

Neither Kinsted nor Lantern has direct access to your money. It cannot be used as a corporate asset. It is not exposed to company creditors. Funds can only move between your investment accounts and your personal bank account.

That is how major institutions are structured. It is designed to protect investors. It is one of the reasons the Canadian system is considered among the safest in the world.

Assets stay independently held at Aviso Wealth.

This is how major banks and investment firms protect client assets.

Neither Lantern nor Kinsted can use your money as a corporate asset.

At Kinsted, investment decisions are made through an investment council where experienced professionals debate ideas, challenge assumptions, and vote on portfolio construction.

13 professionals. Different backgrounds. Different experience levels. Different credentials. All with a voice.

That matters because you are no longer dependent on one portfolio manager and all of their personal biases, blind spots, convictions, moods, or grand predictions about the world.

Here, ideas have to survive debate.

Weekly meetings can get intense. Good.

Strong debate often produces stronger outcomes.

A collective process instead of one opinion with a title attached to it.

Ideas have to be defended, debated, and voted on before they shape portfolios.

The whole structure exists to reduce the damage one person can do when they get it wrong.

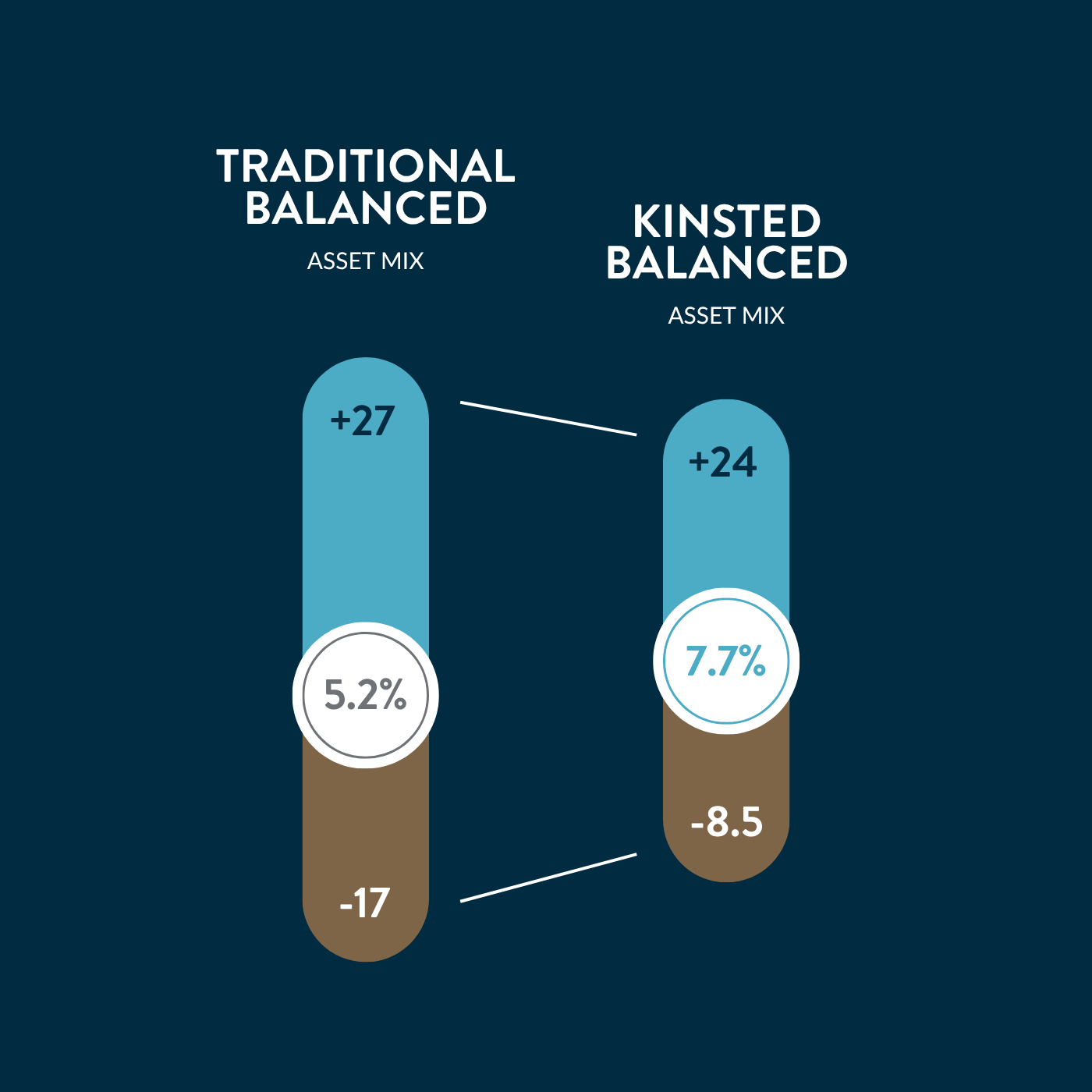

For years, investors have been told that a “balanced” portfolio means 60% equities and 40% fixed income. On paper, it sounds diversified. In reality, it is not.

Today, fixed income can behave much like stocks – it is no longer a safe haven of low volatility. The result is a portfolio that looks diversified but moves as one, you’re just holding different versions of the same exposure.

You are not reducing risk.

That model persists because it’s simple, scalable, and easy for institutions to implement. With Kinsted, the approach is different.

True diversification includes real assets, private businesses, income-producing strategies, and investments across geographies and sectors. The goal is not just to spread money around—but to build a portfolio where each piece plays a distinct role.

That’s how you move from a portfolio that looks balanced… to one that actually is.

The Results

A truly balanced portfolio

Institutional investors often participate in a world retail investors simply cannot access. Kinsted’s structure can open the door to opportunities that were previously out of reach for most Canadians.

Income streams tied to artists like Tim McGraw and Taylor Swift.

How about Los Angeles Dodgers? Because institutional investing is bigger than public stocks and bonds.

A kind of name most families assume belongs to somebody from another World.

Exposure to farmland, food production, and long-term real asset strategies.

Pension funds do not get to think in 90-day chunks.

They have to pay people today, tomorrow, and decades from now. That responsibility forces a different style of investing.

Kinsted applies that same philosophy to client portfolios: diversify broadly, allocate patiently, manage risk carefully, and build for endurance.

The objective is to build a portfolio capable of compounding and supporting wealth across decades.

The Results

Returns comparable to public markets with only half of the volatility

A smarter balance of risk and return.

Compared with a traditional balanced mix, Kinsted Balanced delivered a higher average return with meaningfully lower drawdowns—which means better performance, with less downside.

Kinsted operates as a discretionary portfolio manager, meaning it is legally bound to act in the client’s best interest when making investment decisions.

That is the highest standard of care in financial services. A small percentage of advisors in Canada operate at that level.

Accountability is real. Both the firm and the individual portfolio managers responsible for portfolios are legally responsible for their actions. Violations can lead to penalties, loss of license, or legal action.

In other words: this is professional stewardship of capital, backed by law.

Fiduciary duty is not marketing language. It is enforceable.

Kinsted is managing, not just opining from the sidelines.

The responsibility sits on real people with real legal obligations.

One of the biggest benefits clients feel is simplicity. Your investments are constantly monitored and managed so you can focus on your life instead of babysitting your portfolio.

You do not need to sign documents every time you want to add money. You do not need to fight your way through portals just to move funds. You do not need a circus to take money out for family gifts, travel, or major life events.

If something needs to happen, it usually takes one call, one text, or one email.

You can step away for months and know the structure is still doing its job behind the scenes.

Withdrawals, transfers, and adjustments do not need to become projects.

The experience is built so you do not have to stare at markets all day.

No.

Lantern Wealth is compensated by Kinsted Wealth as a referral partner. Our compensation comes from Kinsted as part of the fee you pay them.

Your portfolio is continuously monitored and managed.

Adjustments are made on your behalf when necessary. The experience is designed to be fully hands-off for clients.

No hard feelings.

The transition can be coordinated to another institution, and we will reimburse any reasonable transfer fees.

One of the most complete investment structures available to Canadian families.

Through Lantern Wealth and Kinsted Wealth, you get access to opportunities and portfolio construction usually reserved for institutions and ultra-large investors — not the standard menu available through banks or retail platforms.

At the same time, you get white-glove planning and advice from Lantern: someone who knows your life, understands your goals, explains things clearly, and is there when you need them.

Behind the scenes, your portfolio is managed by Kinsted Wealth’s investment team, professionals overseeing more than $1.6 billion in assets under strict regulatory oversight and fiduciary responsibility.

Put simply, it is one of the most complete investment structures available to Canadian families.